Blockchain Insurance Solution Development

In traditional insurance, weeks pass between an event and a payout. Bureaucracy, manual verification, high risk of rejection on formal grounds. The insurance company is both judge and interested party. Blockchain solves trust in execution: a smart contract pays out when a condition is met, regardless of the insurer's will. Our team with over 5 years of experience creates such turnkey solutions — from design to audit and deployment. You automate parametric insurance with triggers from Chainlink or build a P2P pool for DeFi risks — we have ready proven architectures. We have implemented over 30 projects, including integration with Chainlink and other oracles. Our smart contracts have passed audits and run in mainnet. Parametric insurance reduces payout time from weeks to minutes — 5 times faster than traditional schemes. Operational cost savings reach 70%.

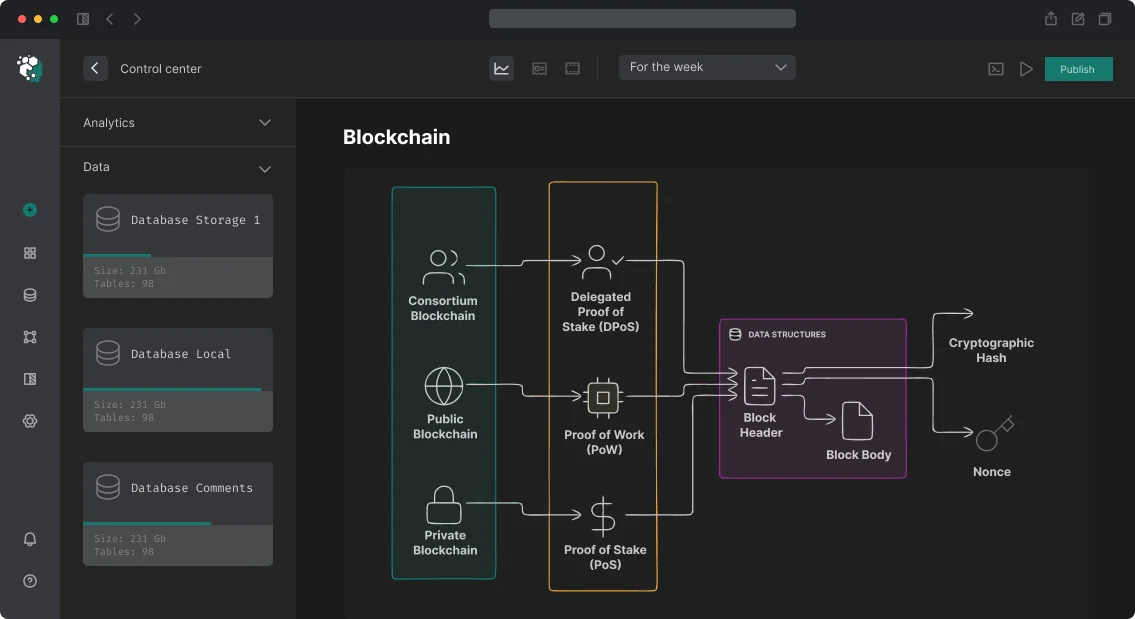

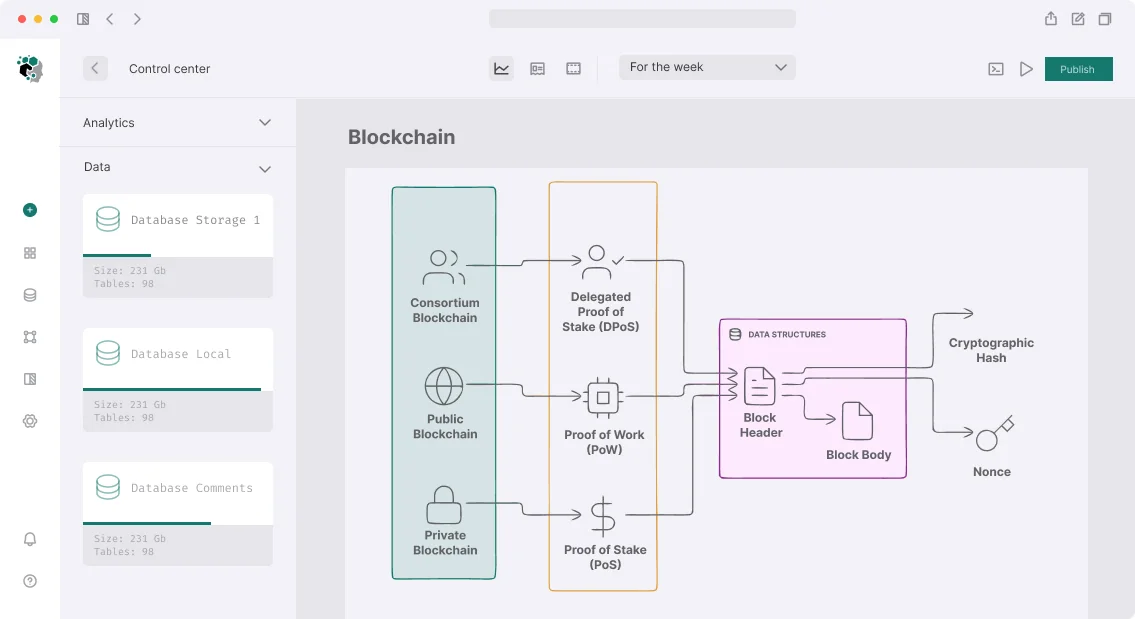

How Does Parametric Insurance on Blockchain Work?

Payout occurs when a measurable parameter is reached — not based on damage, but on a trigger. Classic examples: crop insurance when rainfall is absent, flight delay insurance, crypto asset insurance when price drops below a threshold.

The key element is an oracle that supplies data on-chain. Chainlink provides Data Feeds for prices, Weather Data for weather, Flight Status for aviation. Using aggregated oracles reduces the risk of manipulation.

Example process:

- Deploy a smart contract with a trigger.

- Configure the Chainlink oracle.

- Users purchase policies.

- When the event occurs, the oracle updates data.

- The smart contract automatically pays out.

contract FlightDelayInsurance {

using SafeERC20 for IERC20;

struct Policy {

address policyholder;

bytes32 flightId;

uint256 premium;

uint256 payout;

uint256 departureTime;

PolicyStatus status;

}

enum PolicyStatus { Active, Claimed, Expired, Cancelled }

AggregatorV3Interface public flightOracle;

mapping(bytes32 => Policy) public policies;

function claimPayout(bytes32 policyId) external {

Policy storage policy = policies[policyId];

require(policy.policyholder == msg.sender, "Not policyholder");

require(policy.status == PolicyStatus.Active, "Policy not active");

require(block.timestamp > policy.departureTime + 2 hours, "Too early");

// Получаем данные о задержке из оракула

(, int256 delayMinutes,,,) = flightOracle.latestRoundData();

require(delayMinutes >= 180, "Delay threshold not met"); // 3+ часа задержки

policy.status = PolicyStatus.Claimed;

IERC20(usdcToken).safeTransfer(msg.sender, policy.payout);

emit PayoutExecuted(policyId, policy.payout);

}

}

Parametric insurance is the most successful blockchain model because there is no subjective damage assessment. The condition is either met or not. Development time is 3–5 times less than for P2P pools.

P2P Insurance Pools and Hybrid Models

Participants contribute funds to a common pool. In the event of a claim, payout comes from the pool, and the loss is distributed among the others. Model like Nexus Mutual, InsurAce.

The complexity lies in claim assessment. In DeFi insurance (covering losses from hacks), Nexus Mutual uses token governance: NXM holders vote on each claim. This centralizes the decision but allows evaluating non-formalizable events.

contract InsurancePool {

// Ликвидность пула

uint256 public totalCapital;

// Активные покрытия

mapping(bytes32 => Coverage) public coverages;

// Claim голосование

struct ClaimVote {

uint256 forVotes;

uint256 againstVotes;

uint256 deadline;

bool executed;

}

function submitClaim(bytes32 coverageId, bytes calldata evidence) external {

Coverage storage cov = coverages[coverageId];

require(cov.holder == msg.sender, "Not coverage holder");

require(cov.active, "Coverage not active");

bytes32 claimId = keccak256(abi.encode(coverageId, block.timestamp));

claims[claimId] = Claim({

coverageId: coverageId,

evidence: evidence,

vote: ClaimVote({

forVotes: 0,

againstVotes: 0,

deadline: block.timestamp + 7 days,

executed: false

})

});

emit ClaimSubmitted(claimId, coverageId, evidence);

}

}

Hybrid approach: initial check via oracle (on-chain hack data), final decision through governance for disputed cases. This reduces voting frequency to ~5% of cases.

On-Chain Insurance Product Pricing

Actuarial premium pricing is the most technically nontrivial part. Basic approaches:

| Method | Description | Example |

|---|---|---|

| Fixed premium | Percentage rate of sum, depends on term | 2% per annum |

| Dynamic via AMM | Premium changes by demand curve | Nexus Mutual bonding curve |

| Oracle premium | Premium depends on external factors | Chainlink Functions |

function calculatePremium(

address protocol,

uint256 coverAmount,

uint256 coverDuration

) external view returns (uint256 premium) {

uint256 riskScore = getRiskScore(protocol); // 0-100

uint256 utilizationRate = totalCover * 1e18 / totalCapital;

// Базовая ставка 2% годовых + надбавка за риск

uint256 baseRate = 200; // 2% = 200 bps

uint256 riskMultiplier = 100 + riskScore; // 100-200%

uint256 utilizationMultiplier = 1e18 / (2e18 - utilizationRate); // растёт к 100% utilization

premium = coverAmount * baseRate * riskMultiplier / 10000 / 100

* coverDuration / 365 days

* utilizationMultiplier / 1e18;

}

Managing Insurance Pool Liquidity

Capital providers (LPs) contribute funds and receive a share of premiums. LP risk: large payouts reduce their capital. LP protection mechanisms:

- Coverage ratio — minimum ratio of capital to open covers.

- Withdrawal lock — LP cannot withdraw instantly (usually 7–30 days).

- Reinsurance — part of the risk is reinsured in another pool.

Premium calculation example

Assume a protocol with risk score 30 (out of 100). Cover amount 100,000 USDC for 90 days. Pool utilization 40%. Base rate 2% per annum. Risk multiplier: 100 + 30 = 130%. Utilization multiplier: at 40% utilization = 1e18 / (2e18 - 0.4e18) ≈ 0.625. Premium: 100000 * 200 / 10000 / 100 * 90/365 * 1.3 * 0.625 ≈ 40 USDC.Legal and Compliance Aspects

Insurance is heavily regulated in most jurisdictions. Issuing insurance products without a license is a criminal offense in some countries. Existing blockchain insurance protocols position their products as coverage or protection, avoiding the term insurance. Nexus Mutual operates as a mutual society; Etherisc has obtained insurance licenses in some countries.

When developing a protocol, we consider the operating jurisdiction, type of covered risks, and product structure. Compliance is not optional, especially for products with fiat stablecoin payouts.

Why Oracles Are a Critical Security Node?

An insurance protocol with an oracle creates a specific attack vector: if an attacker can manipulate oracle data, they can trigger payouts. For parametric insurance, this means:

- Using aggregated oracles (Chainlink with multiple data sources). As indicated in the Chainlink documentation, aggregation reduces manipulation risk.

- A time window between the event and the ability to claim (prevents flash loan manipulations).

- Circuit breaker: temporary pause on anomalously large numbers of simultaneous claims.

One documented case: a DeFi insurance protocol paid claims for a "hack" that was actually a controlled exploit by the team itself (exit scam). Without independent on-chain event verification, on-chain insurance can become a tool for fraud.

Comparison of Insurance Models

| Model | Example | Development Complexity | Payout Time |

|---|---|---|---|

| Parametric | Flight delay | Low (3–5 weeks) | Minutes |

| P2P pool | DeFi hacks | Medium (2–3 months) | Days–weeks |

| Hybrid | Parametric + governance | High (3+ months) | Minutes–days |

Our Work Process

- Analysis. Type of risk, jurisdiction, data sources for oracles, claim assessment mechanism, pool tokenomics.

- Design. Pool architecture, premium pricing mechanism, governance, LP liquidity management. Separate compliance structure.

- Development. Foundry with fork tests of mainnet (especially for Chainlink integrations). Fuzz testing of actuarial calculations at boundary values. Invariant testing: total payouts never exceed pool capital.

- Audit. For insurance protocols with real funds — mandatory external audit. Specific vectors: oracle manipulation, governance attacks, bank run scenarios.

- Deployment. Phased launch: limited initial capital, coverage caps, gradual lifting of restrictions after load audit.

What Is Included in Our Work

- Architectural documentation

- Smart contract source code (Solidity, Rust for Solana)

- Integration with Chainlink oracles

- Unit, fuzz, and invariant tests

- External audit results

- Mainnet deployment and configuration

- Client team training

- 12 months of support

Time Estimates

Parametric insurance with a single risk and Chainlink: 3–5 weeks. P2P pool with governance and actuarial pricing: 2–3 months. Full protocol with multiple covers, LP mechanics, and frontend: 3+ months.

The cost is calculated individually — complexity varies from a simple parametric contract to a full protocol. Request a consultation – we will help you choose the optimal architecture. Contact us to discuss your project.